The August Massacre

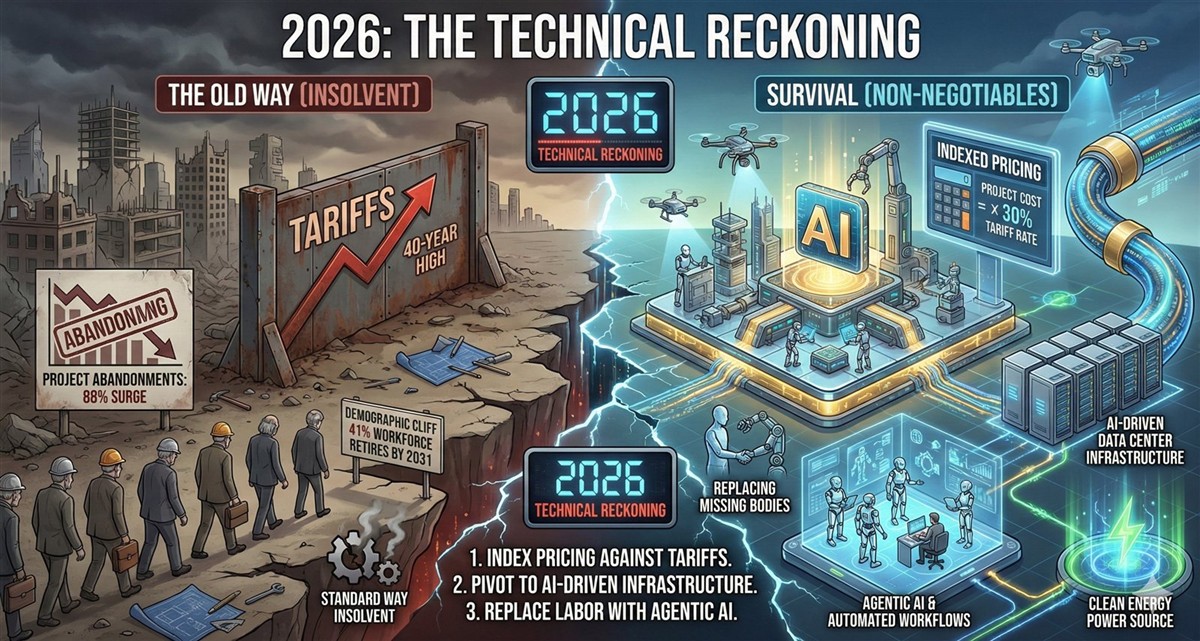

In August 2025, the industry received a collective gut punch: project abandonments surged by 88% year-over-year. Developers didn't walk away because they lost interest; they walked away because the pro formas couldn't survive the collision of 50% steel tariffs and 4.2% wage growth. If you are entering 2026 thinking you can "manage" your way through this with a 5% contingency and a hope that interest rates will bail you out, you’ve already lost the project.

The Deloitte 2026 E&C Outlook confirms what we’ve seen in the mud for twelve months: the margin for error has vanished. We are entering a transition year where capital discipline and technical grit are the only things keeping the lights on.

The Tariff Trap: Building in a Protectionist Economy

We are operating under the highest effective tariff environment in four decades. We aren’t just talking about "supply chain friction" anymore; we are talking about effective rates of 25–30% on construction goods and a staggering 50% on selected steel and aluminum.

For an Owner, this means the "Fixed-Price" contract is becoming a relic or a trap. If your contractor is absorbing these shocks without an escalation clause, they aren't being "partner-friendly"—they are becoming a default risk.

The No-Regret Moves:

Institutionalize Indexing: If your contracts don't have formal pricing indices for materials, you are gambling on geopolitics.

Strategic Stockpiling: We are seeing a return to vertical integration. Smart Owners are buying long-lead gear and raw materials 12 months in advance and paying for storage to hedge against the next tariff hike.

Predictive Procurement: Stop relying on a spreadsheet. Use cloud tools that integrate tariff, freight, and geopolitical data. If you aren’t buying based on predictive cost modeling, you’re just guessing.

The Great Sector Rotation: Data Centers and Energy

Traditional commercial work is soft, with spending down over 8% in late 2025. The smart money has moved. The floor under 2026 demand is being held up by one thing: the insatiable need for AI-related data centers and the energy infrastructure required to cool them.

Large E&C players are repositioning their entire portfolios to chase hyperscale "mega-projects." If you’re a mid-market firm, you can’t credibly chase a $2B data center, but you can pivot toward the regional power and infrastructure upgrades these facilities require.

The Strategic Shift:

Data Center Power & Cooling: This is the new gold rush. The demand isn't just for the shell; it’s for the advanced power-generation and cooling technologies inside.

Reshoring Realities: Manufacturing is still a priority, but it’s cautious. Announcements are high, but groundbreakings are slow due to cost concerns.

Adaptive Reuse: Office-to-residential conversions remain a niche but persistent play for high-vacancy urban cores where the TCO (Total Cost of Ownership) still makes sense.

The Digital Offset: Agentic AI and The End of "Garbage Data"

Deloitte frames digital transformation as the primary offset for margin pressure. This isn't about "going paperless." It's about using Agentic AI—systems that don't just show you a schedule but autonomously re-optimize it in near real-time when a shipment is delayed by a tariff dispute.

We are seeing potential timeline reductions of up to 20% through the integration of BIM, digital twins, and 3D printing. But there is a catch: most AI investments fail because the data quality is garbage.

The Tech Stack for 2026:

Computer Vision: Real-time safety and site monitoring are now standard for federally funded work. If you aren't using vision analytics to track trade progress, you’re relying on "intuition," which is a fancy word for a bad guess.

Digital Twins: Cloud-native twins are no longer a luxury. They are the "Single Source of Truth" required to manage the complex MEP systems in modern energy and data facilities.

AI Agents: We are moving toward AI that manages the "noise"—coordinating trades and anticipating disruptions before the Super even picks up the radio.

The Demographic Cliff: 499,000 Missing Bodies

The labor shortage is no longer a "challenge"; it is a structural failure. In 2026, we will be short approximately 499,000 workers. By 2031, 41% of our current workforce will retire, and only 10% of our pipeline is under the age of 25.

We cannot hire our way out of this. We have to build our way out with fewer people.

The Human Capital Strategy:

Prefabrication & Robotics: If it can be built in a factory, it should be. Reducing on-site labor intensity is the only way to meet the $124 billion in output currently being lost to unfilled positions.

Augmented Training: "Learn-as-you-install" AR workflows are lowering the experience threshold. We don't have five years to train a master plumber; we need AI-assisted tools that make a junior tech as productive as a veteran.

The War for Engineers: We are no longer just competing with the GC down the street. We are competing with Google and Tesla for the same digitally skilled engineers. If your HR strategy doesn't include a digital career pathway, your talent will walk.

“So What?”: The Business Impact of the 2026 Outlook

Financial Impact: Margin compression is the baseline. 88% abandonment rates suggest that carrying costs and material volatility are killing the ROI on traditional builds. Capital discipline and legislative incentives (like the IRA) are mandatory.

Schedule Risk: The 500k-worker gap is a direct threat to schedule integrity. If you aren't using AI-driven scheduling and prefabrication, your substantial completion date is a work of fiction.

Personnel Implications: The "Silver Tsunami" of retirements means a massive loss of institutional knowledge. Capturing that knowledge in digital systems now is a survival requirement.

Strategic Consequences: 2026 is a transition year. Firms that harden their supply chains against tariffs and pivot their portfolios toward energy/data will outperform. Those clinging to the 2019 playbook will be acquired or dissolved.

The Bottom Line

The Deloitte Outlook isn't a suggestion; it’s a weather report for a hurricane. We are moving from a labor-intensive industry to a digitally augmented ecosystem. You can complain about the tariffs, you can lament the retirement of your best Supers, and you can ignore the AI "hype"—but the market won't care.

In 2026, the Owner who controls the data controls the asset. The math no longer mirrors the mud; the math mirrors the model. Build with resilience, or don't build at all.

Actionable Strategy for Owners:

Audit Your Tariff Exposure: If you don't know the "effective tariff rate" on your current CAPEX program, find out by Monday.

Demand AI-Driven Scheduling: Stop accepting static Gantt charts. If the schedule doesn't have a "live" logic that accounts for resource scarcity, it’s a marketing document, not a management tool.

Check the Pipeline: Ensure your GC has a documented workforce retention and AR-assisted training plan. "We’ve got guys" is no longer a valid labor strategy.

Pivot to Power: Whether you’re building a hospital or a warehouse, the energy/cooling infrastructure is where the risk and the value live. Over-invest there.

Check out the Deloitte report: https://www.deloitte.com/us/en/insights/industry/engineering-and-construction/engineering-and-construction-industry-outlook.html